Local Government Audit Exposes Problems

Under Montana law, local governments are required to have audits performed. In this process the books are examined for errors and violations of funding accounting principles. Local Government Budgeting Act governs proper accounting.

We found that simple errors were discovered requiring an adjustment to provide a proper accounting. In these cases, the local government accounting was in violation, but only require a minor correction to be in compliance. Failure to perform an audit according to law, provide for penalties against responsible officials under Montana law.

Broadwater County in Montana has been in the news multiple times over the past several years. The citizens exposed fraud that resulted in a felony fraud conviction of a high level employee. Even though it took 8 years to get the conviction, the court ordered restitution of thousands of dollars to the taxpayers of Broadwater County. The judicial branch of Montana ignored the case and politics took precedence over justice. Responsible elected officials were never charged and are still in office.

Many local government officials across Montana have been challenged on being responsible to the citizens. In Glacier County, missing funds were revealed by an outside audit several years ago. That audit showed a substantial amount of errors. The cost of the audit charged to Glacier county was also substantial. Legal challenges against responsible officials in Glacier County are still pending.

The 66th Montana Legislature brought forward legislation based on the problems found in Glacier County. The legislation took a look at examining the accountability of local elected officials. Political maneuvering in the Legislature inhibited getting legislation passed with full accountability.

The fiscal year ends on June 30th of each year. The audit by law has a time frame for completion. At the completion of the audit an exit interview is held between the county officials and the company that performed the audit. This is the beginning of a process that resolves errors and/or violations of government accounting.

In Broadwater County, Denning, Downing & Associates, certified public accountants, have been contracted to perform audits for several years. The final audit report for the fiscal year ending June 30, 2018 was finally submitted for public review after citizens repeatedly asked for a copy. The finance officer of the county declared that the audit was available to the public online, but the current audit was unable to be readily found.

Montana code 2-7-521MCA provides for a time frame for producing the audit report to the people, within 30 days. The report is required to be delivered to the local paper of record. We learned that Broadwater County officials received the audit report on fiscal year ending June 2018 on March 25 2019. The 30 day statutory requirement for the report to be available to the public was not met.

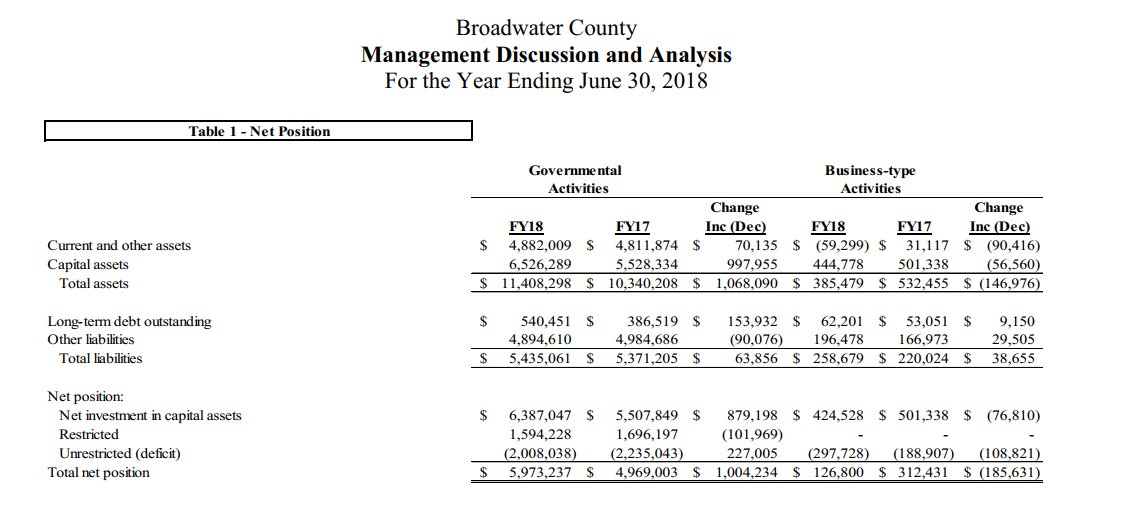

Upon review of the Audit Report, multiple questions arise regarding Local Government Accountability. Note in the report, the County had errors in the Deep Creek Project major fund. They understated $19,504.00, underestimated raw material expenditures of $1,200.00, Federal revenue was overstated $46,260.00, Restatements were understated $65,764.00, expenditures were not coded properly, understating capital outlay and overstating public works expenditures $47,341.00

Expenditures by the county in 2017 were not submitted for reimbursement until fiscal year 2018 and again the same practice was discovered in 2018 and reimbursement not filed until 2019. Recording of project expenditures was found in error as they should have been included as part of capital expenditures.

The control system was not adequate to ensure the grant reimbursement expenditures were recorded as revenue and due from other governments when the expenditures were incurred. The County claims the system was circumvented and coding errors were made when coding project costs.

Because these errors were repeatedly made in a previous audit, the accounting of federal funding requirements on projects in Broadwater County continues to be problematic.

The county made a change in the Solid Waste Fund due to a deficit cash balance at year end. The balanced budget requirement required a short term loan of $179,580.00. The County internal control monitoring procedures should identify when funds revenues are not meeting expenditure needs but failed to reduce expenditures to correct the negative balances. Inadequate monitoring of the financial activity failed to make necessary changes in the expenses to compensate for the reduction of revenues.

At the beginning of fiscal year 2019, the deficit of the Solid Waste fund exceeded $300,000,00. That amount has been reduced with the first half of taxable revenue received. Taxpayers have experienced an increase in the solid waste fee and a reduction in services.

There were errors noted in the health insurance mill levy calculation. 2-9-212 MCA, sets forth the criteria to levy for health insurance contributions the County pays on behalf of employees. The County over levied 6.06 mills for a projected revenue over levied of $69,675.

2018-004 Hazard Mitigation Grant Match (Repeat of finding 2017-001, 2016-001,2015001,2014-003) CFDA Title: Hazard Mitigation Grant Program CFDA Number: 97.039 Federal Award Number: HMGP DR 1996-MT P33R Federal Agency: U.S. Department of Homeland Security Pass-through Entity: Montana Department of Military Affairs

The county was not in compliance with the match requirement as of June 30, 2018 of $71,754 which also resulted in a negative fund balance of $120,413 and a short-term loan from other funds to cover the negative cash balance of $422,986 in the Deep Creek Project major fund.

Due to repeated errors and/or omissions in accounting and reporting of taxpayer dollars, the county continues so see a negative balance in need of attention on behalf of the taxpayers of Broadwater County. The 2018-2019 audit is underway so it will be later in the year or possibly next year before those figures are made available.

The views, opinions, or positions expressed by the authors and those providing comments are theirs alone, and do not necessarily reflect the views, opinions, positions of Redoubt News. Social Media, including Facebook, has greatly diminished distribution of our stories to our readers’ newsfeeds and is instead promoting Main Stream Media sources. This is called ‘Shadow-banning’. Please take a moment and consider sharing this article with your friends and family. Thank you. Please support our coverage of your rights. Donate here: Paypal.me/RedoubtNews